Average True Range Indicator Formula

/ATR-5c535f8fc9e77c000102b6b1.png)

Average True Range Atr Definition

What Is Average True Range Fidelity

Average True Range Atr Chartschool

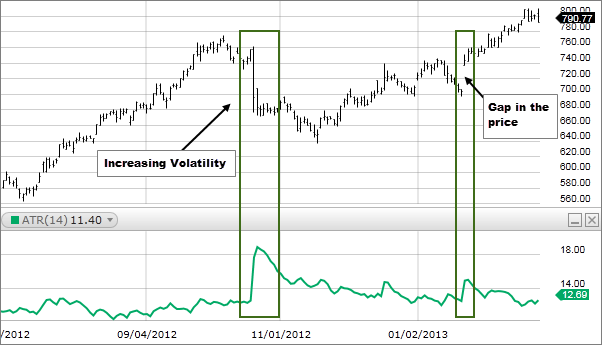

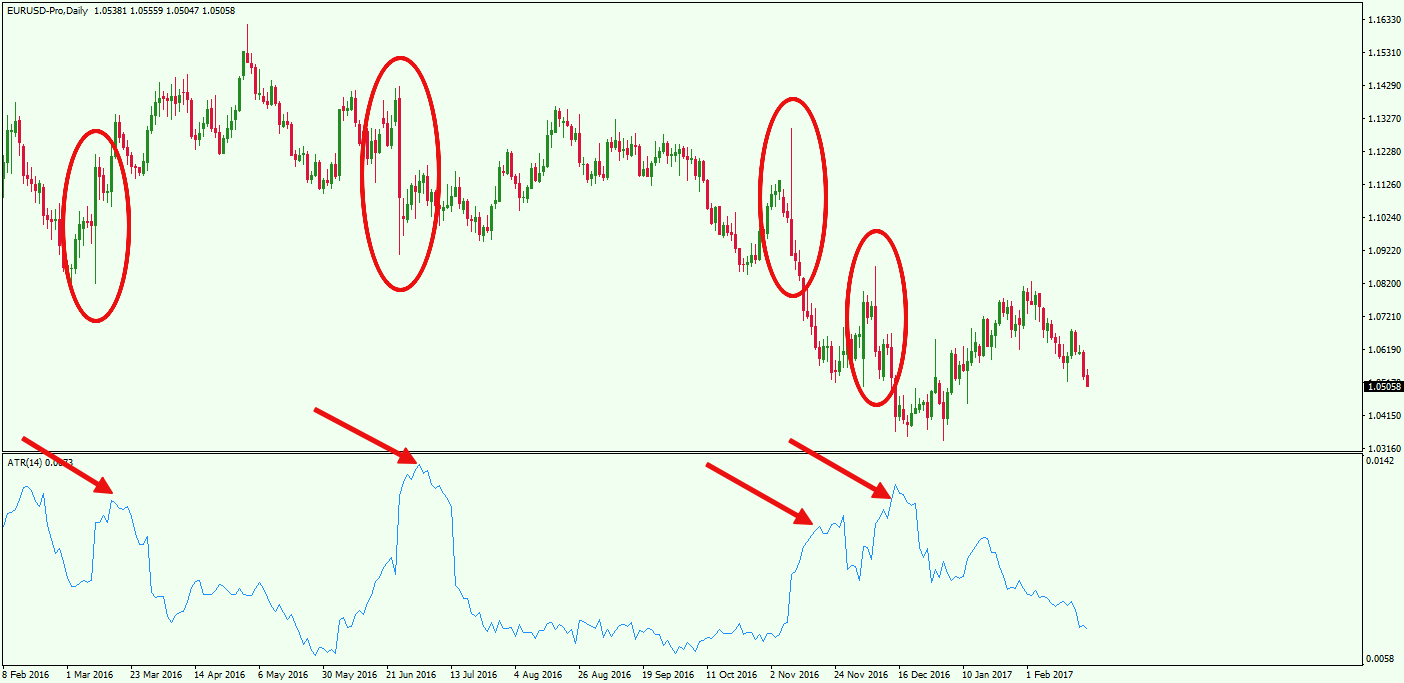

Measure Volatility With Average True Range

How To Use Average True Range Atr Indicator For Optimal Results Forex Training Group

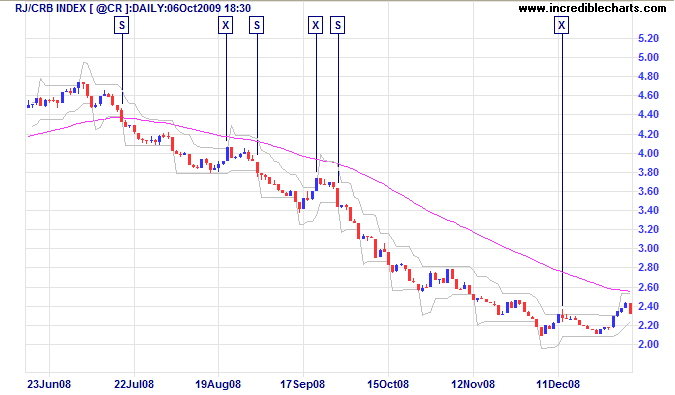

Incredible Charts Average True Range Atr Trailing Stops

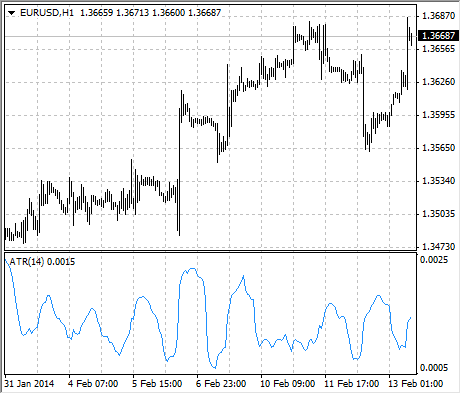

I ve tried to attach a few simple chart examples to better illustrate the point.

Average true range indicator formula.

Incredible Charts Average True Range Atr Bands

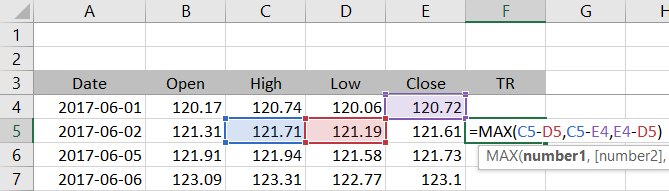

Average True Range Spreadsheet Tutorial

How To Trade Using The Average True Range Indicator

Average True Range Script For Tradingview Pine Kodify

Calculating Average True Range Atr In Excel Macroption

Atr Stop Indicator For Ninjatrader 8 Lizardindicators

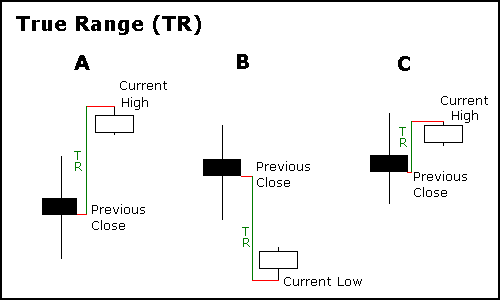

True Range And How It Differs From Range Macroption

The Average True Range Atr Indicator And How To Use It

Atr Average True Range Technical Indicators Youtube

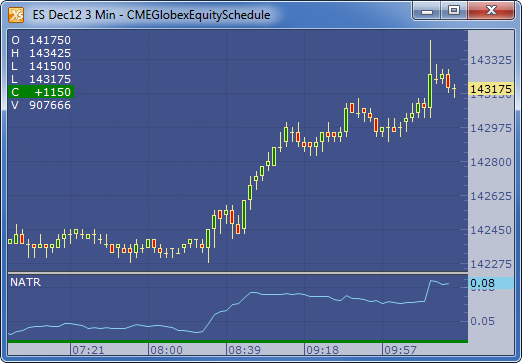

Normalized Average True Range Natr Trading Technologies

Average True Range Atr Technical Indicators Tradingview

Atr Indicator Explained

How To Set A Stop Loss Based On Price Volatility Babypips Com

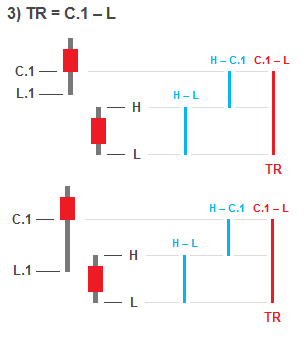

True Range Tr Linn Software

Mt4 Ea Course Atr Stops And Position Sizing Smart Forex Learning

What Is The Atr Indicator How Do You Use It When Trading Mt4

How To Measure Volatility In Forex Babypips Com

Average True Range Technical Indicators Analytics Metatrader 4 Help

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcstlvvu7 3i3s6 Zef2yypdlizeqaij7ds86gnwo2 Khnfistly Usqp Cau

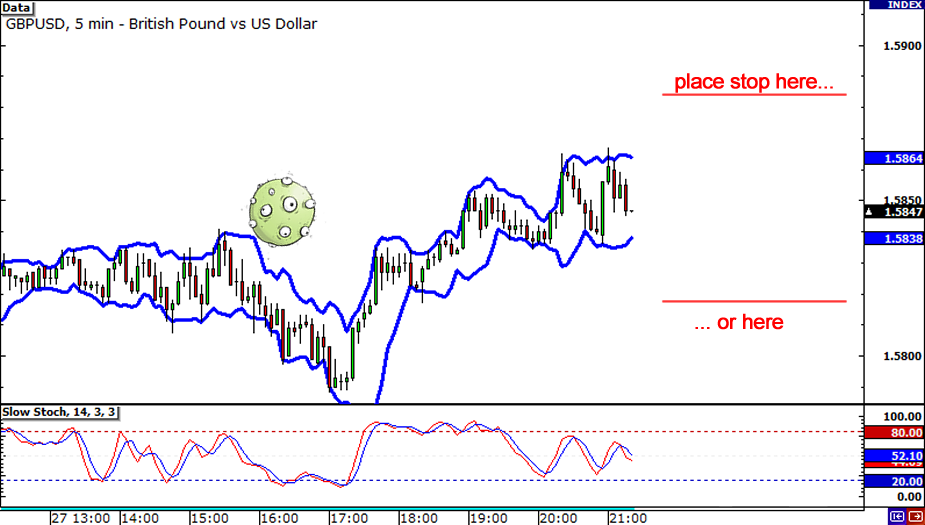

A Logical Method Of Stop Placement

3 Ways To Identify A Ranging Market With Your Algo Quant News

Average True Range Adjusted Barchart Com

A Unique Way To Use Average Daily Range To Your Advantage

How To Use The Average True Range Atr To Set Stops Youtube

Source : pinterest.com